The wording of “water damage caused by a storm” and “flood damage” unfortunately makes it sound like these are the same type of issue. However, that’s far from the case. Although both involve bad weather and catastrophic amounts of water, how insurance companies view these two terms is as distinct types of claims. It’s important to understand each so you know what kind of insurance you need and how to file the appropriate claims.

What Is Water Damage from a Hail or Wind storm?

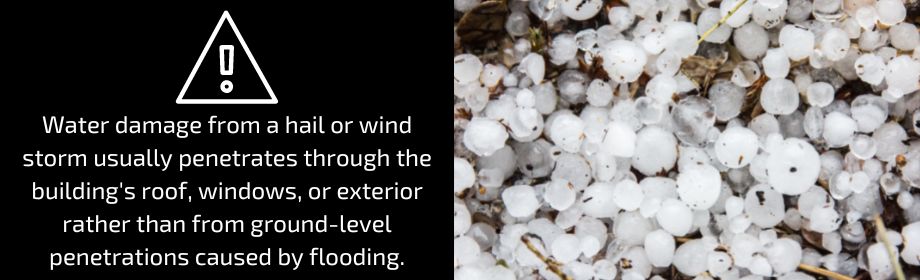

Water damage from a hail or wind storm usually penetrates through the building’s roof, windows, or exterior rather than from ground-level penetrations caused by flooding. For example, if there’s a severe storm with significant rainfall, that could damage your home’s roof. If water leaks in through the damaged areas (roof and windows), it can cause all kinds of damage, including mold, problems with electronics, etc.

Water from wind or hail could also cause damaged pipes, which in turn could lead to leaks that lead to other issues. Another way to describe it is to say that it’s specifically a hail or wind storm that created openings that caused the damage via the water it caused to penetrate the building.

What Is Flood Damage?

The Federal Emergency Management Agency (“FEMA”) describes a flood as something that leads to part or full deluge of two or more acres of land that’s ordinarily dry or two or more properties. Rain can be involved in flood damage, but the shower itself isn’t the primary cause of damage–a resulting flood is. Floods can occur during storms and hurricanes, but they can also result when a nearby rain or storm control basin overflows after slowly building up over time. If your property doesn’t have the correct type of slope for stormwater runoff around the home, that can result in flood damage under certain circumstances.

Does My Homeowner’s Insurance Cover Both Water and Flood Damage?

These are two separate types of claims. Water damage (non-flood) is usually covered in the primary homeowner’s insurance policy and is a widespread type of damage and claim. However, flood damage isn’t covered by basic homeowner’s insurance policies. That’s why it’s important to understand the difference because you could put in a claim for water damage and have it rejected on the grounds that the damage was caused by a flood, not basic water damage.

Is There Any Way to Insure for Flood Damage?

Yes, you have to purchase flood insurance from FEMA through your insurance broker. It’s like adding a separate policy on top of the basic policy. These riders vary from company to company and come with exclusions and deductibles, so it’s worth getting multiple estimates, then reading each one carefully. Because the language can be dense and hard to understand, having an attorney review them can be helpful.

What if I Live in an Area that Frequently Has Floods?

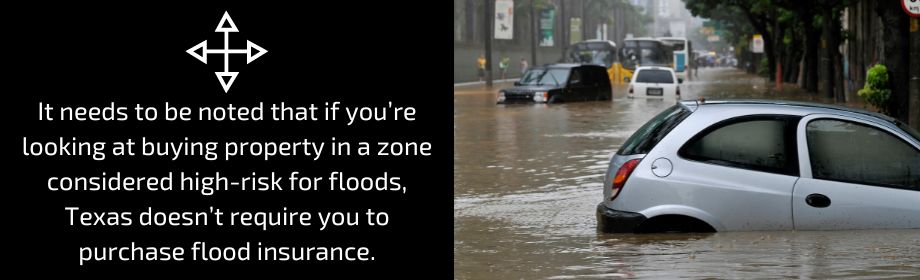

It needs to be noted that if you’re looking at buying property in a zone considered high-risk for floods, Texas doesn’t require you to purchase flood insurance. But then the entire financial risk is your responsibility. Sometimes when purchasing a property in a flood zone, your mortgage company may require you to purchase flood insurance.

That said, for people who live in places where floods are rare, the temptation is to skip flood insurance altogether. Because floods can come from different sources–a hurricane isn’t going to remain at hurricane force once it arrives on the mainland, so someone in central Texas won’t likely get a flood from the hurricane itself. However, as noted above, floods can occur from nearby basin overflows. Living in an area where floods aren’t frequent could make a flood damage rider more affordable and something to be recommended.

What Are “Common Enemy Laws”?

This is a somewhat confusing area of law with important ramifications. In the past, Texas had common enemy rules that said homeowners could do whatever they needed to protect their homes from surface water even if that negatively impacts neighbors. The reasoning was that water and flooding was a “common enemy,” hence the name of the law. For example, if someone created a runoff system on their property that allowed water to bypass their home and flow fully to a neighbor’s property, and that neighbor experienced flooding problems, there was nothing they could do. However, those laws have been changed, and now neighbors who are negatively impacted can seek damages.

That doesn’t mean homeowners can’t work to circumvent the water from their own homes. But they do have to do it in such a way that it won’t be the direct cause of flooding for their neighbors, especially those whose homes may be lower than the other homes.

Will My Auto Insurance Cover Flood Damage to my Vehicle?

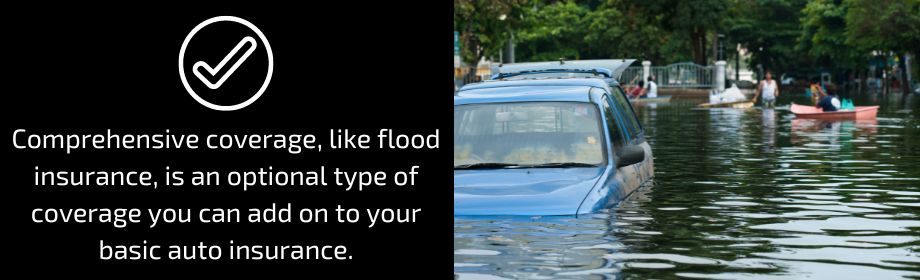

Not always. But if you have comprehensive auto coverage, then yes, your insurance will cover damage to your vehicle done by a flood. Comprehensive coverage, like flood insurance, is an optional type of coverage you can add on to your basic auto insurance.

The basic insurance covers collision, while comprehensive adds protection for floods and other problems that were out of your control, such as theft, fire, vandalism, and weather.

These Texas Attorneys Can Help with Your Storm Damage Insurance Claim

Call us at 855-786-7674 to request a free case evaluation. Our attorneys have extensive experience in working with storm-related water and flood damage. They don’t represent the insurance companies; they represent you and your best interests.